Menu

Close

To provide the best experience, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to provide data such as browsing behaviour or unique IDs on this site. Not consenting or withdrawing consent may adversley affect certain features and fucntions.

Allow AllAtmen automates and derisks certification workflows across renewable fuels, from real-time supply chain data to auditable product claims.

Bring clarity and control to your certification journey, whether you are working in green hydrogen, e-methane, ammonia, biomethane, HVO or SAF.

It’s a challenge for business developers selling a green premium, engineers calibrating supply chains, procurement teams optimising the intake of the right feedstocks, and supply chain managers integrating regulatory constraints into their daily workflows.

With 30+ industrial supply chains already onboarded, Atmen combines frontier technology with deep regulatory expertise to help you stay ahead in a fast-moving certification landscape.

Think of Atmen as the technology layer on top of operational supply chains, enabling continuous compliance and streamlining the official sustainability certification workflows. At scale and across borders.

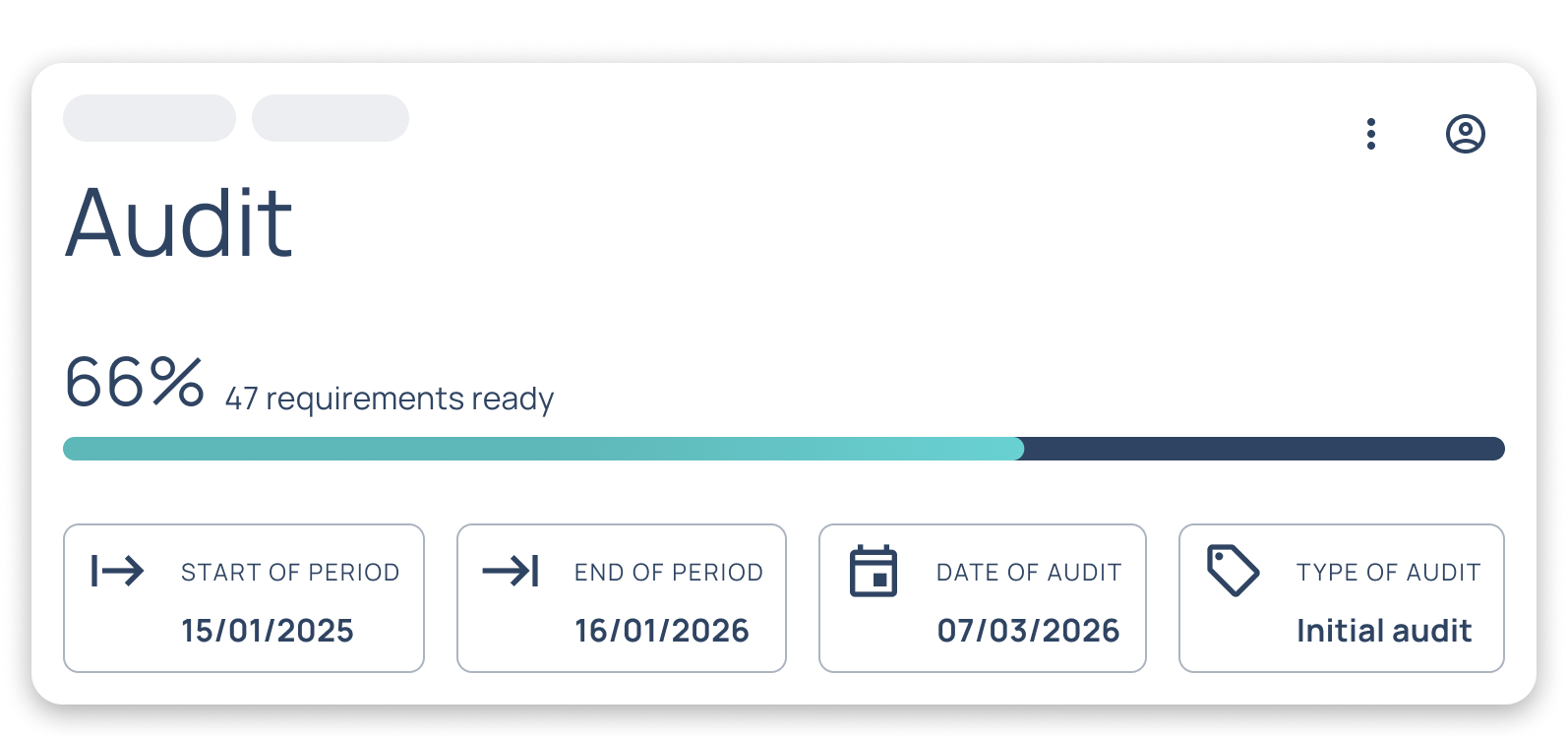

You can manage your entire audit preparation directly in Atmen's platform. This feature helps you collect documents, reconcile data, and generate audit-ready reports, with checklists and reminders based on your certification scheme. Invite external auditors, share granular data, and automatically generate key evidence like mass balances and sustainability proofs.

Saved yearly by our customers

Primary data coverage of key ingredients within first 3 months

(Munich, March 10, 2026) Last week, Germany took a significant step toward closing remaining gaps in renewable fuel regulation. The Bundestag held the first reading of the Second Law on the Development of the Greenhouse Gas Reduction Quota, which will transpose RED III into national law and, for the first time, introduce explicit quotas for green hydrogen and e-fuels in the transport sector.

While most of Europe works toward RED III compliance, industrial offtakers are already demanding certified molecules as regulatory deadlines near. Siemens, Atmen, and TURN2X, all based in Munich, have developed the first end-to-end model for RED III-ready renewable gas production, from automated plant operations to certified product delivery. The plant of the future is already running at TURN2X's first commercial e-methane plant in Miajadas, Spain.

TURN2X produces climate-neutral e-methane by combining green hydrogen with biogenic CO₂. The company plans to scale this model across Europe, aiming to cover 10 percent of Germany’s gas demand by 2031. Miajadas demonstrates the commercial viability of this pathway, with 100 percent of its renewable gas output sold under long-term off-take agreements.

Siemens provides the industrial backbone for this model, including advanced automation systems, digital twin technology for remote plant operation, and standardised, secure deployment of future facilities.

Siemens adopts an ecosystem approach, collaborating with leading partners such as Atmen rather than developing every component in-house. “This is exactly how we at Siemens want to go forward in renewable energies,” says Philipp Glaser, Siemens Digital Industries. “We want to partner with the best solutions so our customers get innovation, technology, and speed of implementation.”

Atmen, a regulatory technology company, provides the certification data layer. At Miajadas, this enabled the site to reach full RFNBO certification, making automated compliance part of day-to-day operations.

“Certification isn’t a nice-to-have; it’s market access and business case realization,” says Flore de Durfort, CEO of Atmen. “Our platform turns operational data into verifiable, auditable proof that keeps production continuously certification-ready so that renewable fuel producers can scale with confidence.”

For TURN2X, combining Siemens’ industrial technology with Atmen’s compliance layer creates a blueprint for rapid, reliable expansion.

“Scaling across Europe brings two challenges: maintaining operational excellence and meeting increasingly complex certification requirements for renewable fuels,” says Dr. Dominik Schollenberger, CTO of TURN2X. “The Miajadas plant shows that when intelligent operations and built-in compliance come together, e-methane can scale with the reliability our customers expect.”

The three companies share a single goal: scaling green energy production with intelligence, trust, and speed.

The plant of the future isn’t a vision. It’s running today in Miajadas.

About TURN2X

TURN2X develops and operates projects using its proprietary technology to produce e-methane by combining biogenic CO₂ with green hydrogen. The company focuses on scalable, infrastructure-ready renewable gas solutions that support industrial decarbonization and energy security.

About Siemens

Siemens AG (Berlin and Munich) is a leading technology company focused on industry, infrastructure, mobility, and healthcare. The company’s purpose is to create technology that transforms everyday life for everyone. By combining the real and the digital worlds, Siemens empowers customers to accelerate their digital and sustainability transformations, making factories more efficient, cities more livable, and transportation more sustainable. A leader in industrial AI, Siemens leverages its deep domain know-how to apply AI – including generative AI – to real-world applications, making AI accessible and impactful for customers across diverse industries. Siemens also owns a majority stake in the publicly listed company Siemens Healthineers, a leading global medical technology provider pioneering breakthroughs in healthcare. For everyone. Everywhere. Sustainably. In fiscal 2024, which ended on September 30, 2024, the Siemens Group generated revenue of €75.9 billion and net income of €9.0 billion. As of September 30, 2024, the company employed around 312,000 people worldwide on the basis of continuing operations. Further information is available on the Internet at www.siemens.com.

About Atmen

Atmen (atmen.co) is a regulatory technology company providing the data infrastructure that powers trusted certification of industrial products. Atmen focuses on automating certification and enabling large-scale, verifiable supply chain transparency across energy-intensive industries.

Founded in January 2023 by energy and regulation experts Flore de Durfort, Quentin Cangelosi, and Erika Degoute, Atmen has raised €6.3M to date to build technology that certifies industrial goods, starting with renewable gases.

Headquartered in Munich, the company's platform is deployed across industrial sites in 9 countries, automating certification workflows and enabling verifiable proof of product attributes throughout the supply chain.

As regulations evolve, they introduce new frameworks, the most recent of which is low-carbon gases under the Gas Directive.

In our recent webinar, co-hosted with CertifHy, we covered what this new low-carbon framework means for producers already navigating RFNBO certification, and how to ensure they’re capturing the additional certifiable value to its full potential.

Think of certification labels like the stickers on a box of juice: the same box can carry several labels (EU Bio, Demeter organic, and so on), each with its own criteria for what qualifies and its own methodology for monitoring. While green gases have international labels too (US, UK, ISO), we'll focus on the European labels in this article.

Until recently, for Europe that meant one label: RFNBO, Renewable Fuels of Non-Biological Origin, defined under the Renewable Energy Directive. Now a second label has joined it: Low-Carbon Fuels (LCF), defined under the Gas Directive.

RFNBO and low-carbon are both clean fuel standards, and in the EU framework every clean fuel standard rests on the same three pillars: an emission threshold, a set of allowed production pathways, and a methodology for calculating emissions.

Low-carbon covers fuels from sources that still cut emissions by at least 70% against the fossil baseline. Two pathways qualify:

In both cases, hydrogen qualifies if its carbon intensity sits below 28.2 gCO₂e/MJ.

That overlap raises an obvious question for anyone already running an RFNBO project: do you pick one label, or run both? We put that question directly to our webinar audience, the poll numbers made one thing clear:

70% of attendees said they expect their organization to pursue both RFNBO and low-carbon pathways, against 9% RFNBO-only, 5% low-carbon-only, and 14% still undecided (2% Other).

The stacked pathway is already the market's default assumption. Here's what's driving that, and what it takes to get there.

.png)

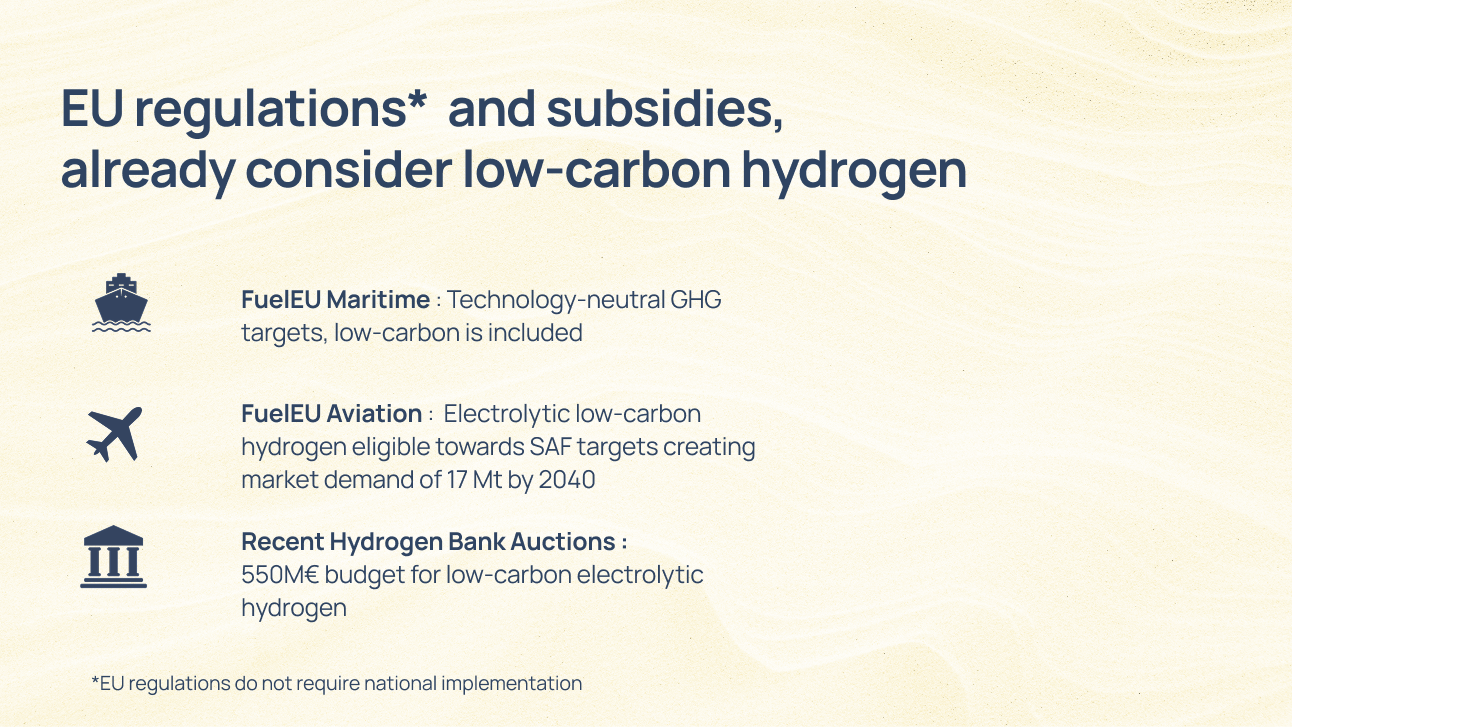

What’s the actual demand for low-carbon fuels?

Demand is currently forming across two channels: EU-level regulations (directly applicable, no national implementation needed) and national implementations of EU directives.

At EU level, two regulations, accompanied by financial support, are already treating low-carbon hydrogen as eligible:

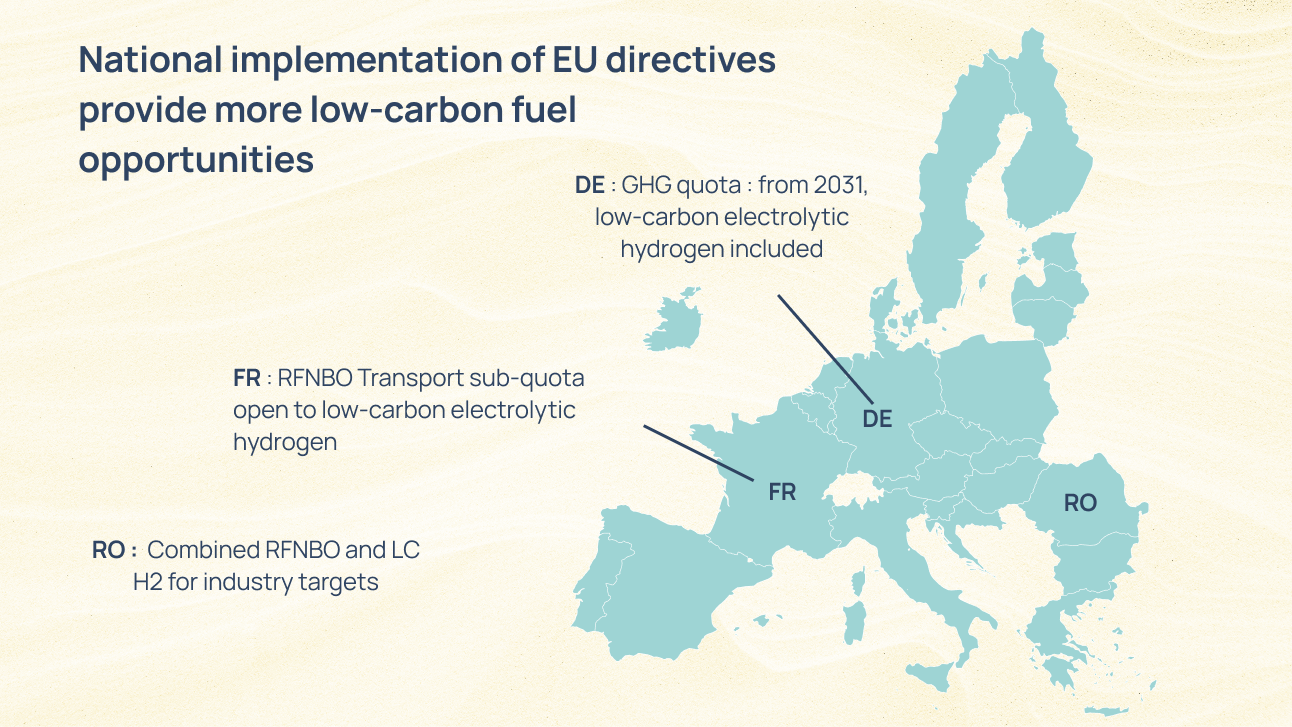

At national level, where the biggest risk of producers overlooking the new label currently sits, and where some of the highest near-term market potential is:

There's a market, and there's production potential. But while the demand pull is getting clearer, willingness to pay remains an open question. That makes low-carbon business cases harder to build with confidence today.

But what are the steps? How does low-carbon integrate into your current setup?

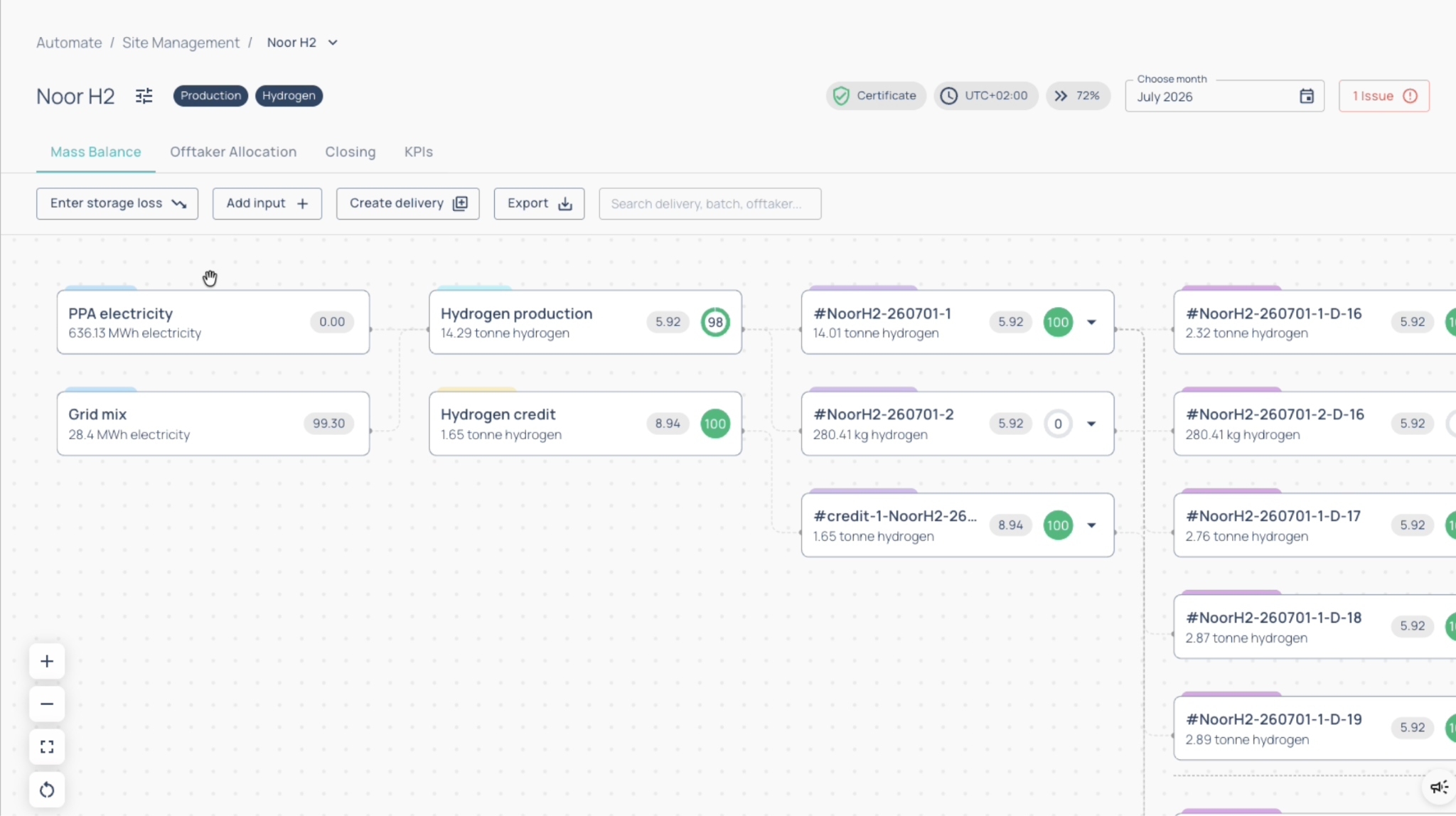

Under RFNBO alone, if your input is 50% renewable (i.e. RFNBO Delegated Acts compliant) and meets the 70% GHG-saving threshold, you get 50% RFNBO output and 50% non-certifiable output. The remaining half of the electrolyzer's production sits outside the certifiable perimeter, uncredited.

With low-carbon now in the picture, that second stream can now be certified too. A typical electrolyzer suddenly has two certifiable output streams rather than one.

On Automate, this shows up concretely: A typical mass balance with a PPA plus a grid mix will highlight a gray portion, say, 280 kg of non-renewable output that was previously uncertifiable.

Under the low-carbon framework, that same volume can now qualify, provided it's documented correctly. And the last point is not optional: documentation is the whole game

This is where preparation matters most. As Emma Andersson, Product Manager at CertifHy highlighted during the webinar:

"If a producer waits until the end of the production period to organize all of the required evidence, they may only find out at the end that certain volumes actually can't be certified or for some reason the documentation is incomplete."

The remedy is upstream: set up your data and traceability correctly before the production month closes, before the audit begins, and ideally before commissioning.

What's left is making the certification actually happen, and, under this new label, a combined audit for RFNBO and low-carbon is possible.

Documents have already been submitted to the Commission, and await approval towards the end of the year. CertifHy additionally plans to offer pre-certification for low-carbon before formal recognition, the same de-risking approach they took with RFNBO.

That means producers can start engaging with the process now rather than wait for 2027.

The practical advantage of combined audits is that they don't double your workload: one certificate can list both scopes across all fuels produced, with a single site visit and merged audit plans, rather than two parallel processes.

Where the two schemes align: system boundaries, allocation logic, mass balance approach, and risk-based auditing.

Where they diverge: RFNBO enforces strict renewable-electricity sourcing rules, while low-carbon is governed by lifecycle GHG intensity without the same renewability test.

Separate rulebooks still apply to GHG calculations, evidence checks, and final claims; the two labels remain distinct even within the same audit.

How can you prepare for a combined RFNBO and low-carbon audit? Early planning is critical for project economics.

Certification planning should begin during the feasibility study phase to align with and inform project design and supply chain decisions.

Before FID: your plant design already determines what you can certify. Metering concepts, the electricity you're buying, how flexible your supply is, and the time granularity all lock in certain outcomes before you've broken ground.

This is where pre-certification is worth using: a check to see whether your planned setup is eligible before you commit to it. It's a tool that's already de-risked plenty of RFNBO projects, and CertifHy is extending the same option to low-carbon.

After FID, during commissioning: this is when your data management and traceability concept needs to be fully built out, not sketched. It matters even more for low-carbon than it did for RFNBO alone, because you're now tracking more data streams, knowing the renewable-versus-grid share of every consignment is what determines which label each molecule earns.

Around COD, at the initial audit: one key lesson from RFNBO experience is worth repeating here. We've seen projects book auditor hours, get everyone lined up, and then discover weeks before the audit that the auditor hadn't actually completed RFNBO training. The same risk exists again with low-carbon, as it's a dedicated training track in its own right.

Preparing for the audit:

Certification timing and audit readiness directly affect commercialization; having the right evidence and structure in place in advance is key.

During the audit, the auditor will check when electricity was consumed, which electricity source was used, whether the renewable electricity rules were met, how greenhouse gas intensity of the production was calculated, and how the resulting output is actually allocated between the RFNBO and low-carbon claims.

Now that the we’ve unraleved the audit. Let's take a deeper dive into the regulatory nitty-gritty of the Low-Carbon Delegated Act (LCDA).

While the 70% GHG threshold requirement stays under the LCDA, electricity no longer has to be renewable. So the practical question becomes, in which countries can you actually produce hydrogen from the grid and still qualify?

The grid carbon intensity values published in the Low Carbon Delegated Act show several countries could operate with 100% grid electricity, considering sufficient efficiency*. The Nordics, who were always in play, but now also joined by Denmark, France and Lithuania.

*Electrolyzer efficiency considered is 70%

The benefits: lower Levelized Cost of Hydrogen (LCOH), lower stack degradation, and better ability to meet offtaker needs. And, to put it in volume terms:

France shows the biggest upside, allowing up to 69% more certifiable output due to high nuclear electricity in the grid. While its neighbor, Germany, for example, can still unlock roughly 10% more.

We’ll be keeping France as our case study to analyse another possible layer of optimization under the LCDA, hourly grid CI.

The country grid average gives you one layer of optimization. The LCDA adds another: hourly grid carbon intensity (CI), based on a defined methodology incumbent to the transmission system operators (TSOs). This lets producers capture the greener hours, when the grid CI dips below its annual average, and translate them into a lower CI.

We ran France as a case study, first week of May 2026:

The results?

Even though a French electrolyser could run baseload and still qualify, operating flexibly on hourly CI lets it capture an even lower carbon intensity. And lower CI already commands a premium in markets like the Netherlands and Germany.

That's a double effect: better project economics and lower environmental impact.

In parallel production with RFNBO, hourly carbon intensity is not yet possible. The RFNBO Delegated Act doesn't allow the hourly methodology, and applying two different methodologies to the same production would return two different results. While the Commission has signaled this will be adjusted, and industry voices have called it a no-brainer, the change hasn't taken place yet.

Also still pending: the consultation on nuclear PPAs, originally expected on June 30, which had not yet launched at the time of publication.

Two moving pieces of regulation worth tracking.

If you want to explore what dual RFNBO + low-carbon certification would look like for your specific setup, reach out to the team.

Both are EU clean fuel standards resting on the same three pillars: an emission threshold, a set of allowed production pathways, and a methodology for calculating emissions. The key difference is electricity sourcing. RFNBO requires renewable electricity and a 70% GHG saving against the fossil baseline. Low-carbon covers fuels produced from non-renewable sources, including grid electricity or fossil sources with carbon capture, that still achieve the same 70% GHG saving and a carbon intensity below 28.2 gCO₂e/MJ. RFNBO certifies the origin and CI of the electricity; low-carbon certifies the carbon intensity of the output.

Yes. One electrolyser may produce both, provided the different shares are correctly calculated, documented and traced.

The RFNBO share depends on the portion of energy input that qualifies as renewable. The remaining output may qualify as low-carbon if it separately meets the low-carbon GHG and traceability requirements.

A combined audit does not double the workload. One certificate can list both scopes, with a single site visit and a merged audit plan. The two schemes share the same system boundaries, allocation logic, mass balance approach, and risk-based auditing methodology.

Where they diverge is in GHG calculations, evidence requirements, and final claims: RFNBO enforces strict renewable electricity sourcing rules, while low-carbon is governed by lifecycle GHG intensity without the same renewability test. One critical practical requirement: confirm that your auditor has completed the dedicated training track for low-carbon to avoid last-minute delays.

As early as the feasibility study phase. Plant design determines what you can certify: metering concepts, electricity sourcing arrangements, flexibility provisions, and temporal granularity all lock in certain outcomes before ground is broken. Pre-certification, available through CertifHy for both labels, is a useful check at this stage to confirm eligibility before FID. After FID, during commissioning, data management and traceability systems need to be fully built, not sketched — because distinguishing the renewable and grid share of every consignment is what determines which label each molecule earns.

Possibly, however some of the hourly batches that would be excluded from RFNBO might still qualify as low-carbon depending on the grid attributes

You will have one audit, with a double-trained auditor checking both scopes. Of course, ensuring proper side-by-side documentation will be required, to avoid double counting.

No EU rule requires separate tools.

One mass balance, documenting the attributes of the outputs should suffice (RFNBO vs low-carbon vs uncertified). Additionally, documentation should explain how each GHG calculation is performed.

Yes.The selected electricity-emissions method must be applied consistently during the calendar year. Switching methods mid-year to obtain a more favourable result is not supported by the regulation.

Yes. Projects outside the EU may qualify if they meet the relevant EU production, GHG, documentation and traceability requirements.

© Copyright Atmen 2024 and Beyond

Designed By The Sourdough

© Copyright Atmen 2023 and Beyond

Designed By The Sourdough